It’s the big day.

The day you go to the title or escrow company, sign your name on the dotted line, hand over a check and prepare to take ownership of your new home.

It’s also the day that you and the seller will pay “closing” or settlement costs, an accumulation of separate charges paid to different entities for the professional services associated with the buying and selling of real property.

It’s too often a day filled with uncertainty and stress.

To help you better understand this confusing subject, the Land Title Association has answered some of the questions most commonly asked about title, closing and closing costs.

You will usually be paying for such things as real estate commissions, appraisal fees, loan fees, escrow charges, advance payments such as property taxes and homeowner’s insurance, title insurance premiums, pest inspections and the like.

The amount you pay for closing costs will vary; however, when buying your home and obtaining a new loan, an estimate of your closing costs will be provided to you pursuant to the Real Estate Settlement Procedures Act after you submit your loan application. This disclosure provides you with a good faith estimate of what your closing costs will be in the real estate process. An itemized list of charges will be prepared when you close your transaction and take title to your new property.

No, and it is easy to understand why. Many different parties will have fulfilled their responsibilities and be awaiting payment upon closing. The title or escrow company will disburse money to those parties, pursuant to the escrow instructions, when funds are available.

Your closing funds should be in the form of a cashier’s check, issued by an institution from the state of your purchase, made payable to the title company or escrow office in the amount requested. A personal check may delay the closing or may be unacceptable to the title or escrow company. An out-of-state check could also cause a delay in your closing due to possible delays in clearing the check.

This point is often misunderstood. Although the title company or escrow office usually serves as a meeting ground for closing the sale, only a small percentage of total closing fees are actually for title insurance protection.

Your title insurance premium may actually amount to less than one percent of the purchase price of your home, and less than ten percent of your total closing costs. The title policy is good for as long as you and your heirs own the property with the payment of only one premium.

Both you and your lender will want the security offered by title insurance.

Your home is an important purchase, and you will want to be certain your home is yours, all yours. Title insurance companies insure your rights and interests in order to protect you against claims.

Your lender is looking to insure the enforceability of their lien on your property and marketability. What is meant by “marketability”? Local lenders will originate a loan here, and, often, sell it to an out-of-state investor. This investor, who may never see the property, needs to know that he has a valid and enforceable lien. Title insurance is the way of making certain. Without a current title policy, the loan is essentially unmarketable.

Title insurers, unlike property or casualty insurance companies, operate under the theory of risk elimination.

Risk elimination can only be accomplished after an intensive period of risk identification.

Title companies spend a high percentage of their operating revenue each year collecting, storing, maintaining and analyzing official records for information that affects title to real property. The issuance of a title insurance policy is highly labor-intensive. It is based upon the maintenance of a title “plant” or library of title records, in many cases dating back over a hundred years. Each day, recorded documents affecting real property are posted to these plants so that when a title search on a particular parcel is requested, the information is already organized for rapid and accurate retrieval.

Trained title experts are able, with the aid of their extensive title plants, to identify the rights others may have in your property, such as recorded liens, legal actions, disputed interests, rights of way or other encumbrances on your title. Before closing your transaction, you can seek to clear those encumbrances which you do not wish to assume.

The goal of title companies is to conduct such a thorough search and evaluation of public records that no claims will ever arise. Of course, this is impossible–we live in an imperfect world, where human error and changing legal interpretations make 100 percent risk elimination impossible. When claims do arise, title insurance companies have professional claims personnel to make sure that your property rights are protected pursuant to the terms of your policy.

To conclude, when you pay for your title insurance policy, you are paying for a team of professionals who have worked together to deliver you a title insurance policy which represents protection for your ownership of real property.

Title or escrow company personnel are available to review and explain your title policy and your closing statement.

Article by CLTA

Stay up to date on the latest real estate trends.

That's the Way the World Goes 'Round

Stalemate is a situation in the game of chess where the player whose turn it is to move is not in check and has no legal move. The game ends in a draw. Since the start… Read more

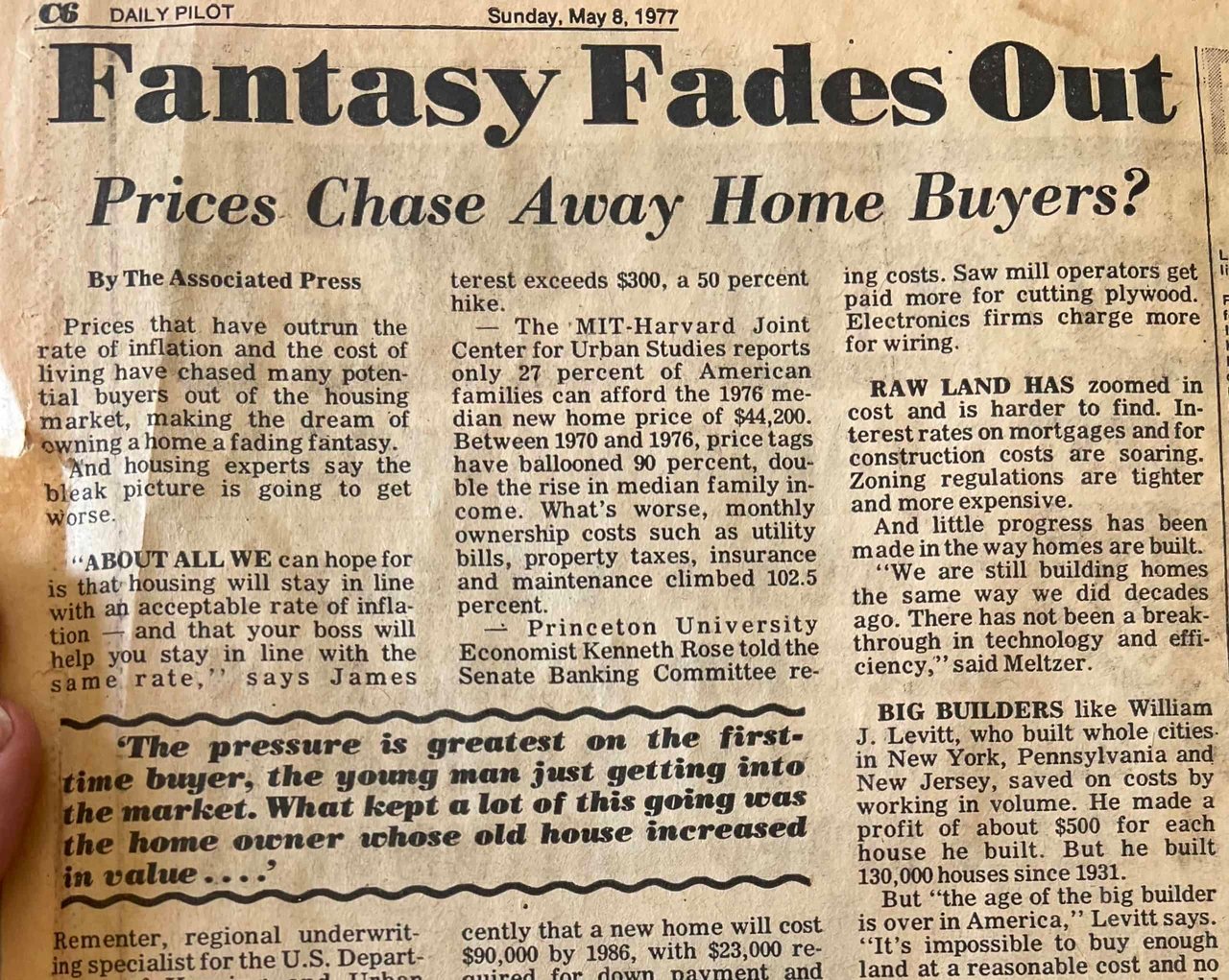

This was the sub-heading of a Daily Pilot article I came across as I was sorting through old archives in a home I recently purchased in Laguna Beach. The article was p… Read more

OFF THE CHARTS When compiling year-over-year statistics, economists tend to work in single-digit percentages. For example, the U.S. GDP growth over the past few years … Read more

2020 Hindsight I know I’m one of the lucky ones. No one in my immediate family has been directly affected by COVID 19, although my father’s 92-year-old twin brother an… Read more

Proposition 19 recently passed, amending California’s Constitution by expanding qualifications for the transfer of a property’s taxable value. Beginning April 1, 2021,… Read more

This year has simply been bonkers. And we still have over a month to go! The news of Kobe and Gianna was swept away by the tsunami of events that followed: the pandemi… Read more

SOUTH ORANGE COUNTY COASTAL HOUSING IN DEMAND Despite the economy being shut down for the majority of 2020, housing along the coast of South Orange County has done exc… Read more

I think we can all agree that a bit of good news is welcome. My gig is working in the residential real estate market, particularly along the coastal towns of South Ora… Read more

You’ve got questions and we can’t wait to answer them.