Lower interest rates have motivated you to refinance your home loan. The lower rate may save you a tremendous amount of money over the life of the loan, but you should also expect to pay the lender the typical closing costs associated with any new loan, including service fees, points, title insurance protection and other expenses.

To the lender, a refinance loan is no different than any other home loan. So, your lender will want to insure that their new loan is protected by title insurance, just as the original lender required. Therefore, when you refinance you are buying a title policy to protect your lender.

Most lenders generate loans and then immediately sell those loans to secondary market investors, such as FannieMae.

FannieMae, in order to protect its security interest in the loan, requires title insurance coverage. Even those lenders who keep original loans in their portfolio are wise to get a lenders policy to protect their investment against title related defects.

Perhaps. Who pays for the lender’s policy on a purchase loan varies regionally and by the terms of individual contracts.

However, even if you did buy a lender’s policy when you purchased your home, the lender’s policy remains in force only during the life of the loan that was insured. If you refinance, the old loan is paid off (the “life” of the loan expires) and a new loan is issued for which the lender will require a new title insurance policy.

When you bought your home, you purchased a Homeowners title policy. The Homeowners’ policy stays in force as long as you or your heirs own the home. When you refinance, your lender will often require that you purchase a new lender’s policy to protect their new security interest in the property. Thus, you are buying a policy to protect your lender, not a new Homeowner’s policy.

Since the time that the original loan was made, you may have taken out a second trust deed on the house or had mechanic’s liens, child support liens or legal judgments recorded against you – events that could result in serious financial losses to an unprotected lender. Regardless if it has been only 6 months or less since you purchased or refinanced your home, a myriad of title defects could have occurred. While you may not have any title defects, many Homeowners do. The only way for a lender to adequately protect itself is to get a new lender’s policy each time you purchase or refinance your home.

Yes. Title companies offer a refinance transaction discount or a short-term rate. Discounts may also be available if you use the same lender for your refinance loan and your original loan. Be sure to ask your title company how they can save you money.

Article by CLTA

Stay up to date on the latest real estate trends.

That's the Way the World Goes 'Round

Stalemate is a situation in the game of chess where the player whose turn it is to move is not in check and has no legal move. The game ends in a draw. Since the start… Read more

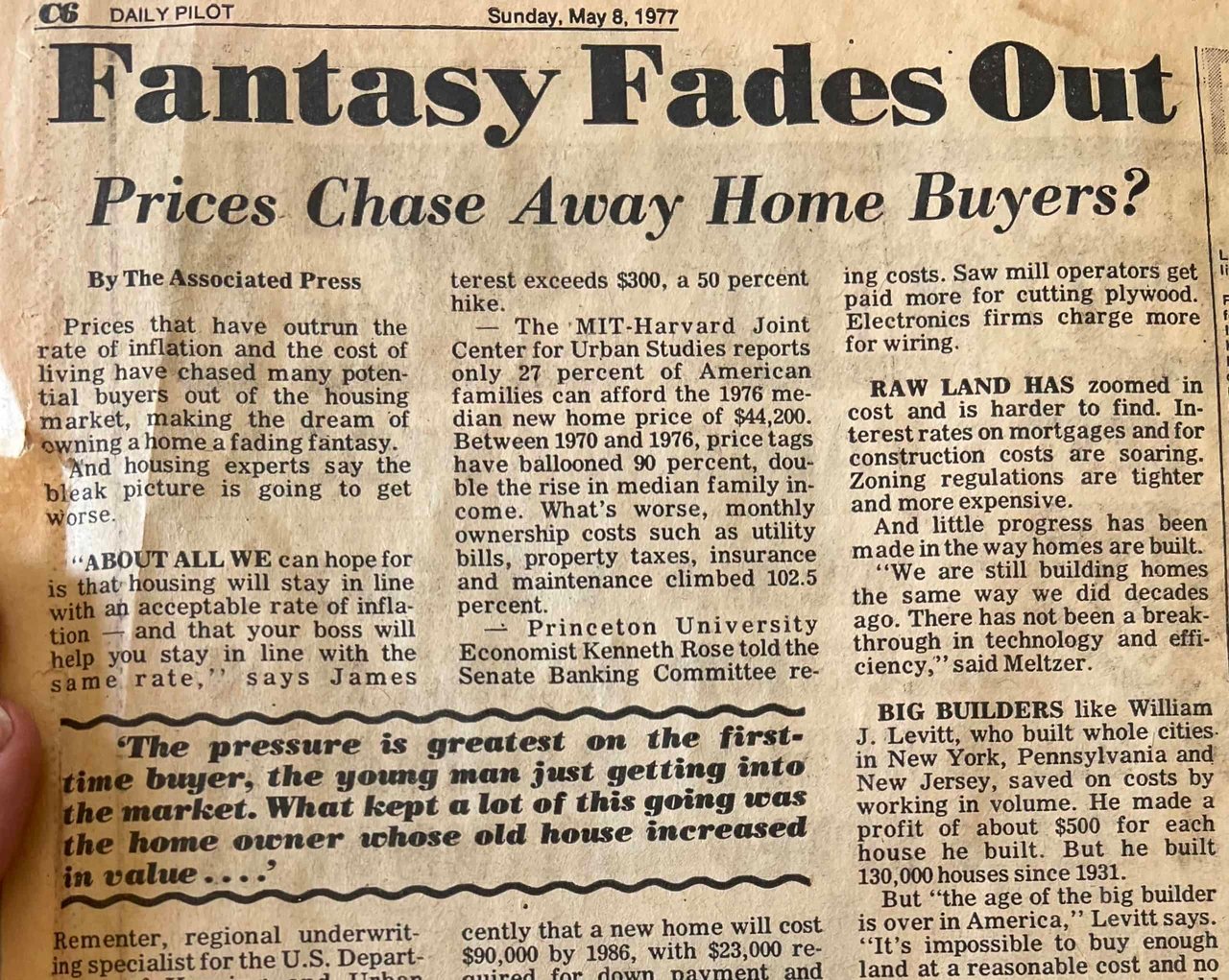

This was the sub-heading of a Daily Pilot article I came across as I was sorting through old archives in a home I recently purchased in Laguna Beach. The article was p… Read more

OFF THE CHARTS When compiling year-over-year statistics, economists tend to work in single-digit percentages. For example, the U.S. GDP growth over the past few years … Read more

2020 Hindsight I know I’m one of the lucky ones. No one in my immediate family has been directly affected by COVID 19, although my father’s 92-year-old twin brother an… Read more

Proposition 19 recently passed, amending California’s Constitution by expanding qualifications for the transfer of a property’s taxable value. Beginning April 1, 2021,… Read more

This year has simply been bonkers. And we still have over a month to go! The news of Kobe and Gianna was swept away by the tsunami of events that followed: the pandemi… Read more

SOUTH ORANGE COUNTY COASTAL HOUSING IN DEMAND Despite the economy being shut down for the majority of 2020, housing along the coast of South Orange County has done exc… Read more

I think we can all agree that a bit of good news is welcome. My gig is working in the residential real estate market, particularly along the coastal towns of South Ora… Read more

You’ve got questions and we can’t wait to answer them.