FICO® stands for Fair Isaac & Company and is the name for the most well known credit scoring system, used by Experian. The credit bureau’s computer evaluates a complete credit profile and assigns a score, which is used to estimate credit worthiness. Each of the three bureaus (Experian, Trans Union, Equifax) employs its own scoring system, so a given person will usually have 3 separate scores. Someone with a higher score will be viewed as a better risk than someone with a lower score. Typically, scores will range from about 600 to 700 or above, although some cases will be outside this range.

There are as many answers to this question as there are loan programs available. Most lenders will take the average of all 3 scores to evaluate an application. Niche loans, such as Easy Qualifier and low down payment loans will have higher FICO® requirements.

The FICO® model has 5 main elements:

Your score can only be changed by the way that item is reported directly to the credit bureaus (Experian, TU, Equifax). Written confirmation from the creditor is required. It is best to make these corrections before you try to purchase a home, because you can never be sure the exact impact a change will have on your score.

You should have your credit reviewed BEFORE you look for a home, and work with a PROFESSIONAL loan officer to make sure your loan is based on the most accurate information.

Stay up to date on the latest real estate trends.

That's the Way the World Goes 'Round

Stalemate is a situation in the game of chess where the player whose turn it is to move is not in check and has no legal move. The game ends in a draw. Since the start… Read more

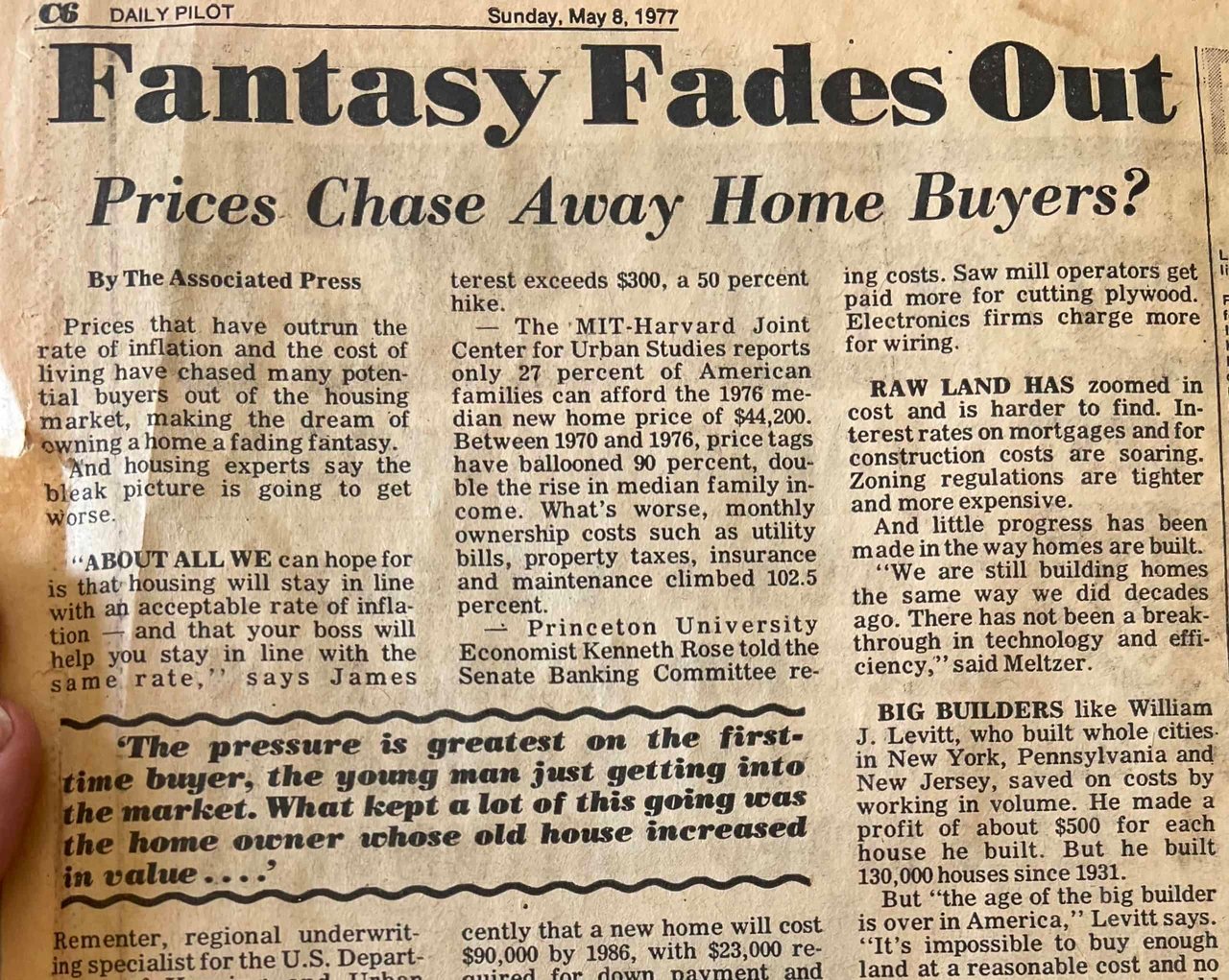

This was the sub-heading of a Daily Pilot article I came across as I was sorting through old archives in a home I recently purchased in Laguna Beach. The article was p… Read more

OFF THE CHARTS When compiling year-over-year statistics, economists tend to work in single-digit percentages. For example, the U.S. GDP growth over the past few years … Read more

2020 Hindsight I know I’m one of the lucky ones. No one in my immediate family has been directly affected by COVID 19, although my father’s 92-year-old twin brother an… Read more

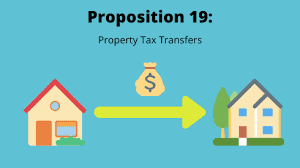

Proposition 19 recently passed, amending California’s Constitution by expanding qualifications for the transfer of a property’s taxable value. Beginning April 1, 2021,… Read more

This year has simply been bonkers. And we still have over a month to go! The news of Kobe and Gianna was swept away by the tsunami of events that followed: the pandemi… Read more

SOUTH ORANGE COUNTY COASTAL HOUSING IN DEMAND Despite the economy being shut down for the majority of 2020, housing along the coast of South Orange County has done exc… Read more

I think we can all agree that a bit of good news is welcome. My gig is working in the residential real estate market, particularly along the coastal towns of South Ora… Read more

You’ve got questions and we can’t wait to answer them.