When preparing to buy a home, the first thing many homebuyers do is look at the real estate ads in newspapers, magazines and listings on the Internet. Some potential buyers read how-to articles like this one. The next thing you should do – before you call on an ad, before you talk to a REALTOR®, before you shop for interest rates – is look at your savings.

Why?

Because determining how much money you have available for down payment and closing costs affects almost every aspect of buying a home – including how you write your purchase offer, the loan programs you qualify for, and shopping for interest rates.

If you only have enough available for a minimum down payment, your choices of loan program will be limited to only a few types of mortgages. If someone is giving you a gift for all or part of the down payment, your options are also limited. If you have enough for the down payment, but need the lender or seller to cover all or part of your closing costs, this further limits your options. If you borrow all or a portion of the down payment from your 401K or retirement plan, different loan programs have different rules on how you qualify.

Of course, if you have enough for a large down payment, then you have lots of choices.

Your loan choices include such varied programs as conventional fixed rate loans, adjustable rate mortgages, buydowns, VA, FHA, graduated payment mortgages and all the varieties of each.

A very important reason you need to have at least some idea of your down payment is for shopping for interest rates. Some loan programs charge a slightly higher interest rate for minimal down payments. Plus, the interest rates for different loan programs are not the same. For example, conventional, VA, and FHA all offer fixed rate loans. However, the rates vary from one program to another.

If you shop lenders by phone, the loan officer will be able to tell you which programs fit and quote your rates accordingly. However, if you are shopping on the Internet, you have to develop some idea of your loan program on your own.

Another reason you need to have a clue about your down payment is because it affects how you write your offer to purchase a home. Not only are you required to put your down payment information in the offer, but also different loan programs have different rules that also affect how you write your offer. This is especially important when dealing with FHA and VA loans.

If you are asking the seller to pay all or part of your closing costs, you have to be certain your loan program allows what you are asking. For smaller down payments, lenders allow the seller to pay less closing costs than for larger down payments. Some loan programs will allow a seller to pay certain types of costs, but not others.

Finally, your down payment also affects your ability to qualify for a loan. When you make a small down payment, lenders are fairly strict about having you conform to their underwriting guidelines. For larger down payments, they will tend to make allowances or exceptions to the rules.

As you can see, the down payment affects every choice you make when you buy a home. Although you should look at ads, familiarize yourself with neighborhoods, learn about prices, and read as much as you can – when you get ready to take action – the first thing you should do is figure out how much money you have available for the purchase.

Stay up to date on the latest real estate trends.

That's the Way the World Goes 'Round

Stalemate is a situation in the game of chess where the player whose turn it is to move is not in check and has no legal move. The game ends in a draw. Since the start… Read more

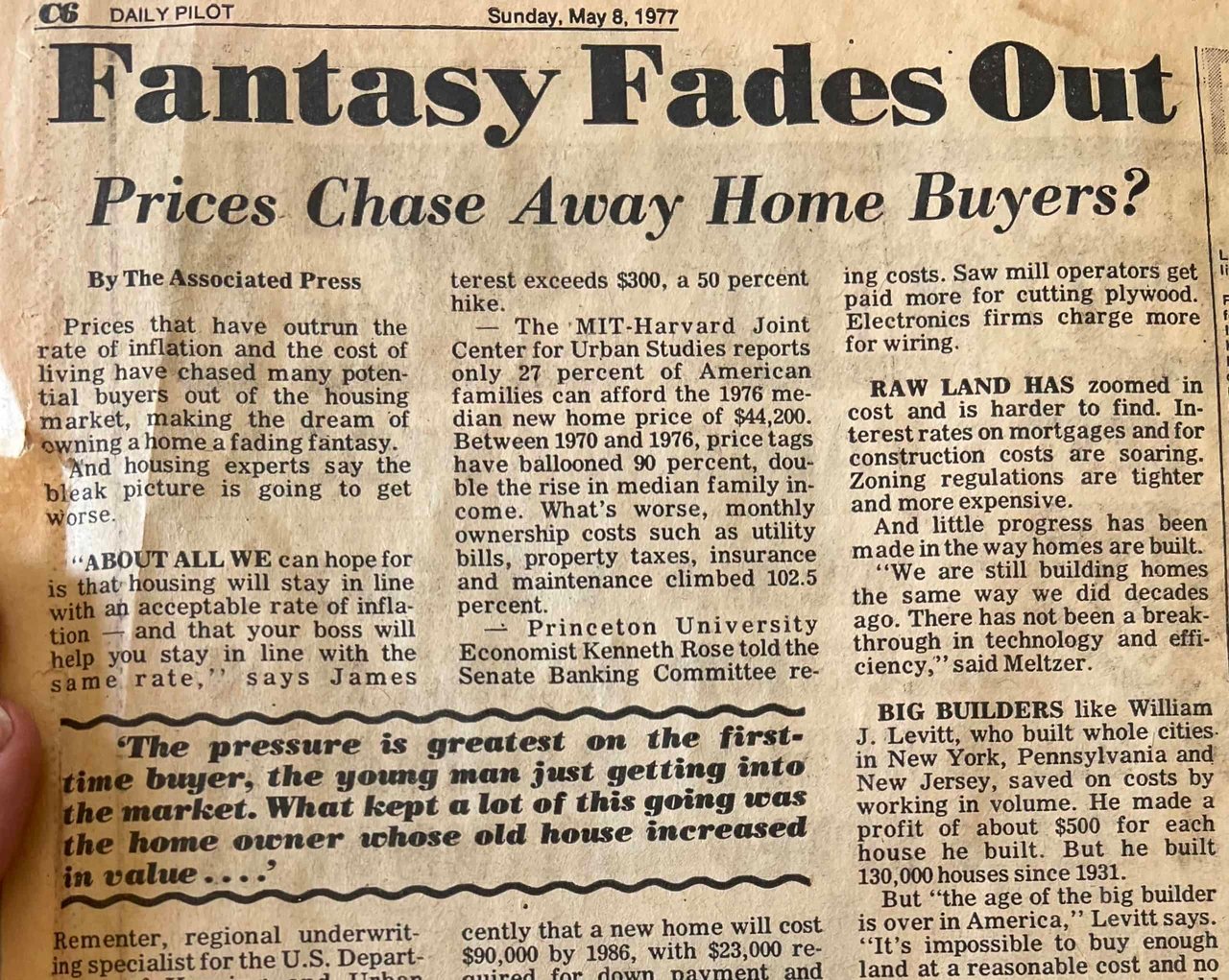

This was the sub-heading of a Daily Pilot article I came across as I was sorting through old archives in a home I recently purchased in Laguna Beach. The article was p… Read more

OFF THE CHARTS When compiling year-over-year statistics, economists tend to work in single-digit percentages. For example, the U.S. GDP growth over the past few years … Read more

2020 Hindsight I know I’m one of the lucky ones. No one in my immediate family has been directly affected by COVID 19, although my father’s 92-year-old twin brother an… Read more

Proposition 19 recently passed, amending California’s Constitution by expanding qualifications for the transfer of a property’s taxable value. Beginning April 1, 2021,… Read more

This year has simply been bonkers. And we still have over a month to go! The news of Kobe and Gianna was swept away by the tsunami of events that followed: the pandemi… Read more

SOUTH ORANGE COUNTY COASTAL HOUSING IN DEMAND Despite the economy being shut down for the majority of 2020, housing along the coast of South Orange County has done exc… Read more

I think we can all agree that a bit of good news is welcome. My gig is working in the residential real estate market, particularly along the coastal towns of South Ora… Read more

You’ve got questions and we can’t wait to answer them.